MENU

05-07-2024

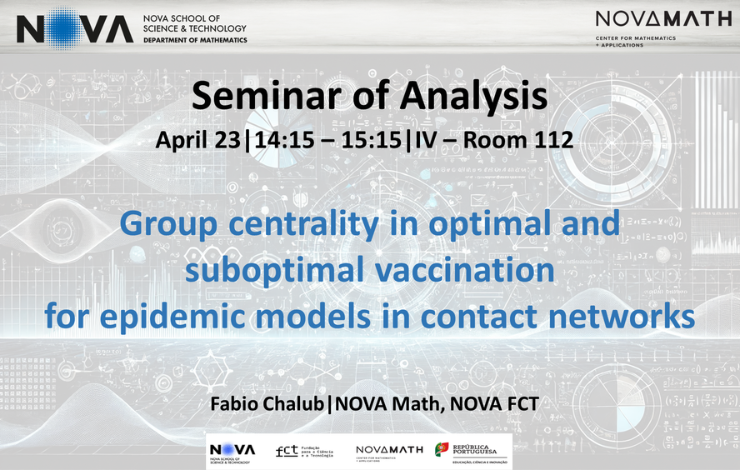

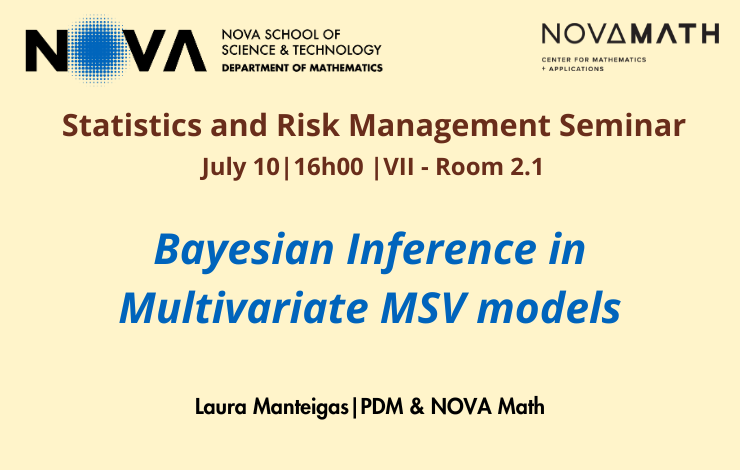

The Center of Mathematics and Applications (NOVA Math), promote the Seminar of Statistics and Risk Management with the title: “Bayesian Inference in Multivariate MSV models". Laura Manteigas (PDM & NOVA Math) is the speaker.

Abstract: Financial time series frequently exhibit serially correlated changes in volatility. While this has led to significant research on multivariate ARCH models, MSV models offer significant statistical benefits. Thereby, this study aims to examine temporal volatility patterns through the latter. The research will employ Bayesian MCMC methodology to estimate MSV models, providing a more comprehensive understanding of the multivariate volatility dynamics (e.g., by deriving the posterior distributions for model parameters and studying the complex relationships between the series). Specifically, it aims to investigate volatility patterns in the emerging markets of the EU (as classified by MSCI) across three distinct periods: before, during, and after the COVID-19 pandemic.

Wednesday 10th July 2024, 16h00.